Py: Socio-Economic Index Construction#

This notebook was originally created by Andres Villegas Ramirez for the Data Analytics Applications subject, as Case study 1 - The Socio-Economic Indexes for Areas in the DAA M06 Unsupervised learning module.

Data Analytics Applications is a Fellowship Applications (Module 3) subject with the Actuaries Institute that aims to teach students how to apply a range of data analytics skills, such as neural networks, natural language processing, unsupervised learning and optimisation techniques, together with their professional judgement, to solve a variety of complex and challenging business problems. The business problems used as examples in this subject are drawn from a wide range of industries.

Find out more about the course here.

Purpose:#

This case study demonstrates the use of principal component analysis (PCA) in the construction of an index to rank the socio-economic status of different geographical areas within a country (in this instance, Australia). Such index can be useful to identify areas that require funding or services, or as input for research into the relationship between socio-economic conditions and other outcomes in different areas.

In Australia, the Australian Bureau of Statistics (ABS) produces four of such indexes, referred to as the Socio-Economic Indexes for Areas (SEIFA). SEIFA ranks areas in Australia based on their relative socio-economic advantage and disadvantage.

This notebook replicates the methodology adopted by the ABS in constructing one of these indexes - Index of Economic Resources, or IER by Statistical Area 1 (SA1).

This Jupyter notebook is organised into the following sections:#

Section 1: Load required packages

Section 2: Define a function for plotting

Section 3: Import and transform data

Section 4: Apply Principal Component Analysis and calibrate SEIFA score

Section 5: Check against ABS publication

1. Load Packages#

# Import required Python packages

#Dataframe operations

import pandas as pd

#PCA

from sklearn.decomposition import PCA

from sklearn.preprocessing import StandardScaler

#Plotting

import matplotlib.pyplot as plt

2. Define Functions#

# Define a function to obtain the explained variances from the PCA features.

## Good practice to define functions upfront.

def plot_explained_variances(pca):

exp_var_pca = pca.explained_variance_ratio_

plt.bar(range(1, len(exp_var_pca) + 1), exp_var_pca, alpha = 0.5, align = 'center',

label='Individual explained variance',color='dodgerblue')

plt.ylabel('Explained variance ratio')

plt.xlabel('Principal component')

plt.legend(loc='best')

plt.tight_layout()

plt.show()

3. Import and Transform Data#

# Import data

## File 1: Standardised socio-economic variables published by the ABS (i.e. input to the PCA model)

## File 2: IER scores by Statistical Area 1 published by the ABS

infolder = 'https://actuariesinstitute.github.io/cookbook/_static/daa_datasets/'

file1 = 'standardised_variables_seifa_2021_cut.csv'

file2 = 'IER_2021.csv'

data1 = pd.read_csv(infolder + file1)

data2 = pd.read_csv(infolder + file2)

# Inspect data

## These are numerical features (e.g. % corresponding to a variable, see dictionary below) which are standardised

data1.head()

| SA1_2021 | INC_LOW | INC_HIGH | ATSCHOOL | ATUNI | CERTIFICATE | DEGREE | DIPLOMA | NOYR12ORHIGHER | NOEDU | ... | HIGHCAR | NOCAR | DISABILITYU70 | ENGLISHPOOR | ONEPARENT | SEP_DIVORCED | UNINCORP | CHILDJOBLESS | MORTGAGEOVER30 | RENTOVER30 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 10102100701 | 0.031160 | -0.451226 | -0.307998 | -0.611843 | 2.110423 | -0.792820 | 1.399224 | 0.039552 | -0.494326 | ... | 1.124942 | -0.361674 | 1.160679 | -0.628432 | -0.087881 | -0.046096 | 0.533110 | -0.797863 | 0.427678 | -1.208146 |

| 1 | 10102100702 | -0.745478 | 0.235597 | 0.309750 | -0.718416 | 0.795239 | -0.138695 | 1.122862 | -0.328068 | -0.494326 | ... | 2.165534 | -0.737816 | -1.371078 | -0.628432 | -1.513208 | -0.216841 | 1.846095 | -0.797863 | 0.322564 | -1.208146 |

| 2 | 10102100703 | 0.207462 | -0.333816 | 0.648522 | -0.373289 | 0.143017 | 0.089753 | -0.024178 | -0.148292 | -0.494326 | ... | -0.474119 | -0.425240 | -1.064640 | -0.628432 | 0.078716 | 0.963607 | 0.486319 | -0.335393 | -0.486090 | -0.029516 |

| 3 | 10102100704 | 0.383411 | -0.417133 | -1.082034 | -0.887458 | -0.308372 | 0.417513 | -0.160872 | 0.083635 | 0.108973 | ... | -0.407742 | -0.528653 | 0.038035 | -0.628432 | 0.949299 | 1.482164 | 0.808398 | 0.554274 | -0.156349 | -0.423796 |

| 4 | 10102100705 | 0.334499 | 0.256282 | -1.018268 | -0.396676 | 0.235498 | -0.072269 | -0.227208 | 0.356362 | -0.494326 | ... | -0.135464 | -0.477578 | 0.056221 | -0.628432 | -1.048310 | 1.253986 | 0.795448 | -0.116016 | -0.297469 | -0.292223 |

5 rows × 45 columns

Variable dictionary#

Variable name |

Variable description |

|---|---|

INC_LOW |

Per cent of people living in households with stated annual household equivalised income between \(1 and \)25,999 (approx. 1st and 2nd deciles) |

LOWRENT |

Per cent of occupied private dwellings paying rent less than \(250 per week (excluding \)0 per week) |

NOCAR |

Per cent of occupied private dwellings with no cars |

LONE |

Per cent of occupied private dwellings who are lone person occupied private dwellings |

ONEPARENT |

Per cent of one parent families with dependent offspring only |

OVERCROWD |

Per cent of occupied private dwellings requiring one or more extra bedrooms (based on Canadian National Occupancy Standard) |

UNEMPLOYED_IER |

Per cent of people aged 15 years and over who are unemployed |

GROUP |

Per cent of occupied private dwellings who are group occupied private dwellings |

OWNING |

Per cent of occupied private dwellings owning dwelling without a mortgage |

UNINCORP |

Per cent of dwellings with at least one person who is an owner of an unincorporated enterprise |

INC_HIGH |

Per cent of people with stated annual household equivalised income greater than $91,000 |

HIGHMORTGAGE |

Per cent of occupied private dwellings paying mortgage greater than $2,800 per month |

MORTGAGE |

Per cent of occupied private dwellings owning dwelling (with a mortgage) |

HIGHBED |

Per cent of occupied private dwellings with four or more bedrooms |

# Inspect data

## IER scored published based on 2021 Census data collection

data2.head()

| SA1_2021 | IER_2021 | |

|---|---|---|

| 0 | 10102100701 | 1023.037282 |

| 1 | 10102100702 | 1088.576036 |

| 2 | 10102100703 | 986.1022032 |

| 3 | 10102100704 | 965.4964701 |

| 4 | 10102100705 | 1013.432808 |

# Select variables ABS uses to calibrate the IER (per their methodology)

variable_IER = [

'SA1_2021',

'INC_LOW',

'LOWRENT',

'NOCAR',

'LONE',

'ONEPARENT',

'OVERCROWD',

'UNEMPLOYED_IER',

'GROUP',

'OWNING',

'UNINCORP',

'INC_HIGH',

'HIGHMORTGAGE',

'MORTGAGE',

'HIGHBED'

]

data1_IER = data1[variable_IER]

# Inspect data type for these variables

data1_IER.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 59430 entries, 0 to 59429

Data columns (total 15 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 SA1_2021 59430 non-null int64

1 INC_LOW 59427 non-null float64

2 LOWRENT 59400 non-null float64

3 NOCAR 59422 non-null float64

4 LONE 59430 non-null float64

5 ONEPARENT 59319 non-null float64

6 OVERCROWD 59417 non-null float64

7 UNEMPLOYED_IER 59429 non-null float64

8 GROUP 59430 non-null float64

9 OWNING 59423 non-null float64

10 UNINCORP 59430 non-null float64

11 INC_HIGH 59427 non-null float64

12 HIGHMORTGAGE 59400 non-null float64

13 MORTGAGE 59423 non-null float64

14 HIGHBED 59422 non-null float64

dtypes: float64(14), int64(1)

memory usage: 6.8 MB

# Remove rows with missing values

print(data1_IER.isna().sum())

data1_IER_dropna = data1_IER.dropna()

SA1_2021 0

INC_LOW 3

LOWRENT 30

NOCAR 8

LONE 0

ONEPARENT 111

OVERCROWD 13

UNEMPLOYED_IER 1

GROUP 0

OWNING 7

UNINCORP 0

INC_HIGH 3

HIGHMORTGAGE 30

MORTGAGE 7

HIGHBED 8

dtype: int64

# Standardise data for PCA

## Select data from column 2 onwards (inclusive). First column is SA1 ID.

pca_data = data1_IER_dropna.iloc[:, 1:]

## Standardise these columns to mean 0 and variance 1

sc = StandardScaler()

sc.fit(pca_data)

pca_data = sc.transform(pca_data)

## Inspect outputs, each row represents a SA1

print(data1_IER_dropna[50:55])

print(pca_data[50:55])

SA1_2021 INC_LOW LOWRENT NOCAR LONE ONEPARENT OVERCROWD \

50 10102100921 -0.694978 -0.149470 0.026395 2.161618 0.016894 0.614584

51 10102100923 -0.399570 -0.230663 -0.392438 0.346039 0.479932 -0.327006

53 10102100925 -1.184584 -0.369694 -0.584525 1.995606 1.010923 0.163947

54 10102100926 -0.755434 0.636737 0.194704 1.770099 -0.418760 0.828480

55 10102100927 -0.534872 -0.113768 -0.443336 -0.248692 -0.929502 0.042116

UNEMPLOYED_IER GROUP OWNING UNINCORP INC_HIGH HIGHMORTGAGE \

50 -0.768433 -0.298797 -1.379936 -1.409706 0.565708 -0.711816

51 -0.502225 -0.435782 -0.068099 -1.078581 0.417556 -0.309550

53 0.393123 0.492720 -1.552475 -0.869567 0.401089 -0.914661

54 0.562322 1.018832 -1.283807 -0.853606 -0.501616 -0.914661

55 -0.591322 0.001803 -0.652794 -0.622710 0.248079 0.145029

MORTGAGE HIGHBED

50 -0.075949 -1.407022

51 0.780225 0.198026

53 -0.382142 -1.473097

54 -1.468772 -1.443632

55 0.547895 0.465557

[[-6.97384349e-01 -1.49102654e-01 2.73842498e-02 2.18456511e+00

1.68271418e-02 6.21443888e-01 -7.82538918e-01 -3.01193486e-01

-1.38687638e+00 -1.42934823e+00 5.65712045e-01 -7.14208804e-01

-8.01255787e-02 -1.41014150e+00]

[-4.00578528e-01 -2.30600290e-01 -3.93807726e-01 3.52373086e-01

4.80225191e-01 -3.29406608e-01 -5.11392783e-01 -4.39108873e-01

-7.01834243e-02 -1.09373813e+00 4.17385805e-01 -3.11130864e-01

7.79986710e-01 1.96337876e-01]

[-1.18930828e+00 -3.70152778e-01 -5.86976088e-01 2.01703428e+00

1.01162817e+00 1.66375413e-01 4.00564091e-01 4.95697733e-01

-1.56005434e+00 -8.81893199e-01 4.00899556e-01 -9.17462999e-01

-3.87727179e-01 -1.47627516e+00]

[-7.58127412e-01 6.40055426e-01 1.96640397e-01 1.78946385e+00

-4.19164718e-01 8.37443911e-01 5.72902051e-01 1.02538267e+00

-1.29039226e+00 -8.65715951e-01 -5.02866086e-01 -9.17462999e-01

-1.47935650e+00 -1.44678433e+00]

[-5.36520854e-01 -1.13266264e-01 -4.44992083e-01 -2.47800227e-01

-9.30303140e-01 4.33461879e-02 -6.02142493e-01 1.44766450e-03

-6.57042865e-01 -6.31693191e-01 2.47710087e-01 1.44364950e-01

5.46588117e-01 4.64107182e-01]]

4. Modelling#

This section performs the PCA to recreate the ABS’s IER Index.

# Initiate the PCA.

pca = PCA()

# Fit the PCA model to determine the transformed features.

## It took 2 lines to fit the PCA model.

pca.fit_transform(pca_data)

# Plot variance explained by principal components

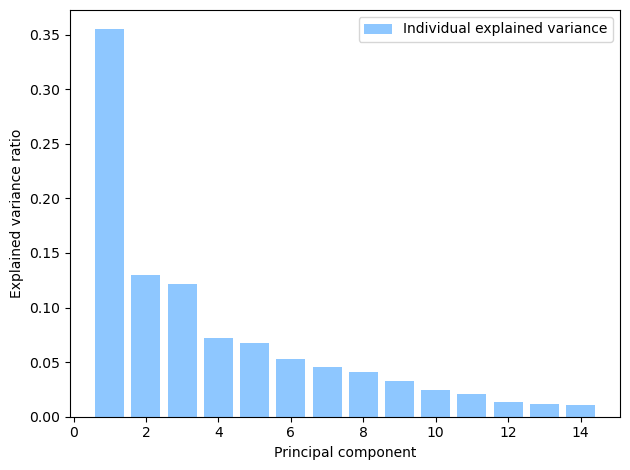

plot_explained_variances(pca)

Principal component 1 (PC1) explains over 30% of the variance in the data. PC1 is used as the basis of calculating the IER.

pca_data[0]

array([ 3.21902216e-02, -1.95351071e-01, -3.62869762e-01, 3.59364682e-01,

-8.80285299e-02, 1.99924572e-01, -6.52078395e-01, -9.12914962e-01,

1.26794033e+00, 5.39782081e-01, -4.52416487e-01, -3.17209382e-01,

2.45495526e-01, 4.39423025e-04])

# Reverse sign (per ABS methodology)

pca_data_transformed = -1.0*pca.fit_transform(pca_data)

# Extract first principal component in a dataframe

pca1 = pd.DataFrame(pca_data_transformed[:, 0], columns = ['IER_2021'])

# Attach SA1 ID to

IER_S1 = pd.concat([data1_IER_dropna['SA1_2021'].reset_index(drop = True), pca1]

, axis=1)

print(IER_S1.head(1))

SA1_2021 IER_2021

0 10102100701 0.517295

# Calculation from first principal

## Sign implies how each variable contributes to a score

## Reverse sign to make it more comprehensive

component_df = pd.DataFrame({

'Variable': data1_IER.columns[1:],

'PC1 Loading': -1.0 * pca.components_[0],

'First SA1': pca_data[0]

})

print(component_df)

raw_score_first_SA1 = (component_df['PC1 Loading'] * component_df['First SA1']).sum()

print('\n')

print('\n')

print(raw_score_first_SA1)

Variable PC1 Loading First SA1

0 INC_LOW -0.327920 0.032190

1 LOWRENT -0.320014 -0.195351

2 NOCAR -0.316516 -0.362870

3 LONE -0.307799 0.359365

4 ONEPARENT -0.243785 -0.088029

5 OVERCROWD -0.231555 0.199925

6 UNEMPLOYED_IER -0.217694 -0.652078

7 GROUP -0.175738 -0.912915

8 OWNING 0.152087 1.267940

9 UNINCORP 0.211586 0.539782

10 INC_HIGH 0.233597 -0.452416

11 HIGHMORTGAGE 0.285636 -0.317209

12 MORTGAGE 0.295868 0.245496

13 HIGHBED 0.334995 0.000439

0.5172947202278048

A recap of the dataframe operations for transforming raw data to principal components#

Dataframe name |

Operations |

|---|---|

data1 |

Raw data we’ll be using to replicate the SEIFA IER score, numercial features (%) |

data1_IER |

Select features for determining IER from data1 |

data1_IER_dropna |

Remove missing values in data1_IER |

pca_data |

Standardise features in data1_IER_dropna to mean 0 and s.d. 1, used to perform PCA |

pca |

Output of PCA, Principal Components |

pca_data_transformed |

Reverse sign in pca |

pca1 |

Extract first principal component from pca_data_transformed |

IER_S1 |

Attach SA1 identifier to pca1, compared to dataframe ABS_IER_S1 which is the published data |

# Standardise calibrated IER scores to mean of 1,000 and standard deviation of 100 (per ABS methodology)

IER_S1['IER_recreated'] = (IER_S1['IER_2021']/IER_S1['IER_2021'].std())*100+1000

print(IER_S1.tail())

SA1_2021 IER_2021 IER_recreated

59298 90104100401 0.022187 1000.995399

59299 90104100402 -0.055935 997.490510

59300 90104100403 -0.785740 964.748521

59301 90104100404 -1.702813 923.604956

59302 90104100407 -0.116936 994.753789

5. Reconcile with ABS publication#

# Extract first two columns in the desired data type

ABS_IER_S1 = data2.iloc[:, [0, 1]]

ABS_IER_S1['IER_2021'] = pd.to_numeric(ABS_IER_S1['IER_2021'],

errors='coerce')

ABS_IER_S1['SA1_2021'] = pd.to_numeric(ABS_IER_S1['SA1_2021'],

errors='coerce', downcast = 'integer')

print(ABS_IER_S1.info())

print('\n')

print(ABS_IER_S1.head())

print('\n')

print(ABS_IER_S1.isna().sum())

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 59421 entries, 0 to 59420

Data columns (total 2 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 SA1_2021 59421 non-null int64

1 IER_2021 59303 non-null float64

dtypes: float64(1), int64(1)

memory usage: 928.6 KB

None

SA1_2021 IER_2021

0 10102100701 1023.037282

1 10102100702 1088.576036

2 10102100703 986.102203

3 10102100704 965.496470

4 10102100705 1013.432808

SA1_2021 0

IER_2021 118

dtype: int64

## Remove rows with missing value

print(ABS_IER_S1.isna().sum())

ABS_IER_S1_dropna = ABS_IER_S1.dropna()

print(len(data1_IER_dropna))

print(len(ABS_IER_S1_dropna))

SA1_2021 0

IER_2021 118

dtype: int64

59303

59303

# Merge the recreated with the published data for reconciliation 1 - histograms

join = pd.merge(ABS_IER_S1_dropna, data1_IER_dropna, how = 'left', on = 'SA1_2021')

# Plot histogram of calibrated IER scores

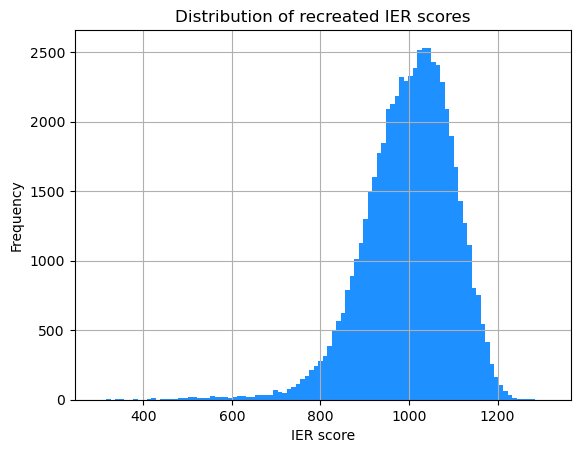

IER_S1.hist(column='IER_recreated', bins=100, color='dodgerblue')

plt.title('Distribution of recreated IER scores')

plt.xlabel('IER score')

plt.ylabel('Frequency')

plt.show()

# Plot histogram of publisehd IER scores

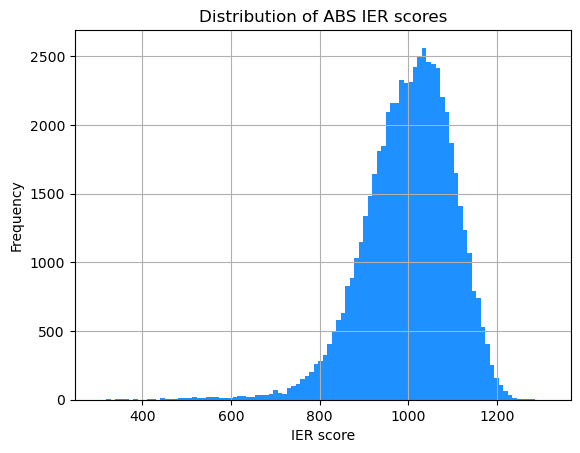

ABS_IER_S1_dropna.hist(column='IER_2021', bins=100, color='dodgerblue')

plt.title('Distribution of ABS IER scores')

plt.xlabel('IER score')

plt.ylabel('Frequency')

plt.show()

ABS_IER_S1_dropna.to_csv('check_ABS_IER_S1_dropna.csv')

The two histograms are very similar in shape!

# Extract columns we need

IER_S1_reduce = IER_S1[['SA1_2021', 'IER_recreated']]

# Merge the recreated with the published data for reconciliation 2 - scatter plot

IER_join = pd.merge(ABS_IER_S1_dropna, IER_S1_reduce, how = 'left', on = 'SA1_2021')

print(IER_join.tail())

SA1_2021 IER_2021 IER_recreated

59298 90104100401 1000.369129 1000.995399

59299 90104100402 996.979765 997.490510

59300 90104100403 964.139169 964.748521

59301 90104100404 923.050144 923.604956

59302 90104100407 994.377312 994.753789

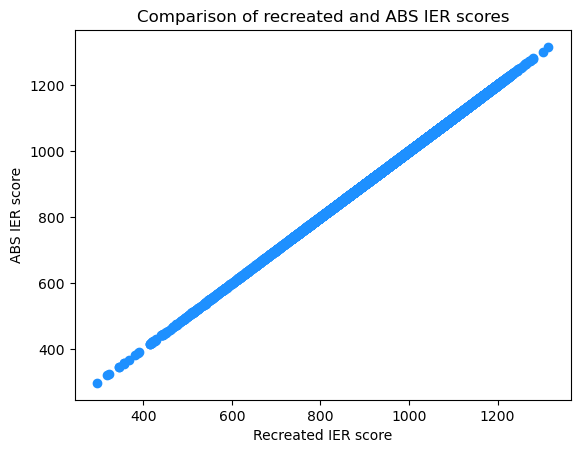

# Plot calibrated score vs. published score

plt.scatter('IER_recreated', 'IER_2021', data = IER_join, color='dodgerblue')

plt.title('Comparison of recreated and ABS IER scores')

plt.xlabel('Recreated IER score')

plt.ylabel('ABS IER score')

plt.show()

The above scatter plot shows that the two sets of indexes are very closely aligned.